It's Free to Speak to an Advisor, 7 days, 8am - 10pm

It's Free to Speak to an Advisor, 7 days, 8am - 10pm

Combining incomes with your parents could help you secure the home you want. We can help with:

Please complete the form accurately so that we can get a better picture of your financial situation.

Yes, you can get a joint mortgage with a parent. This option allows you to combine your income with that of your parent, potentially increasing your borrowing capacity and improving your mortgage eligibility.

Lenders will assess both applicants’ income, expenses, and credit history to determine affordability. It’s important to note that while both parties are responsible for the mortgage repayments, only one, typically the child, is listed as the property owner. This arrangement can be beneficial for young buyers struggling to meet the affordability criteria on their own.

With a joint mortgage, parents can support their children’s homeownership journey without holding a long-term stake in the property. This type of mortgage is sometimes referred to as a joint borrower sole proprietor mortgage.

Our Customers Rate us 4.9/5

A joint mortgage with your parents works by combining financial resources to enhance your borrowing potential. Both you and your parent(s) will be evaluated by the lender, who will examine income, outgoings, and creditworthiness to ensure affordability.

Although both parties are equally liable for mortgage repayments, only the child’s name appears on the property’s title deed. This means the parent does not have an ownership interest in the property.

Lenders typically require that the property be the primary residence of the child, and the parent’s involvement can be adjusted or removed when the child can afford the mortgage independently. This type of mortgage can be particularly useful for first time buyers who need additional financial support to secure a home loan.

Appointments 7 Days a Week

To get a joint mortgage with your parents, you should start by speaking with a mortgage broker to explore your options.

Your mortgage advisor will help you understand the specific criteria each lender has, including age limits, income requirements, and credit scores. Both you and your parent(s) will need to provide detailed financial information for the lender’s assessment.

Once a suitable lender is found, you will apply for the mortgage together. If approved, both parties are accountable for the repayments, even though only the child will be listed as the property’s owner.

This setup allows the parent to exit the arrangement when the child can manage the mortgage independently. It’s also wise to consider the impact on both parties’ credit ratings and ensure you have a clear understanding of the long-term financial commitment involved.

Explore 1000s of Mortgage Options

Our Customers Love Us

![]() 3,500+ 5 Star Reviews

3,500+ 5 Star Reviews

Derek

They were great when handling our mortgage application even though it was a bit different to the normal one. Highly recommended

3 days ago

Michelle

The team at UK Moneyman have been excellent, really informative, providing sound advice with no judgement and supporting the best possible way forward for myself. I would definitely use the team again, they’ve made the whole process simple and...

2 weeks ago

Lawrence

Great company to work with, very helpful and excellent communication. Chris and Jo did a great job with our application. I highly recommend.

2 weeks ago

Gemma

Excellent speedy service and always available to work around the best times for us, including calls at weekends

1 month ago

Gillian

Having dealt with Leo previously I knew I would be getting a brilliant service and a good deal.

1 month ago

Karen

Very helpful.Quick response to any questions or concerns. Selected the right product to meet our requirements.

1 month ago

Stephen

We went to the Moneyman to start with regarding a new mortgage only which went really smoothly and everything was explained in simple terms at our request Malcom made it feel at ease . Once i had the confidence with them we asked them to help with...

1 month ago

What to Expect From the Mortgage Process...

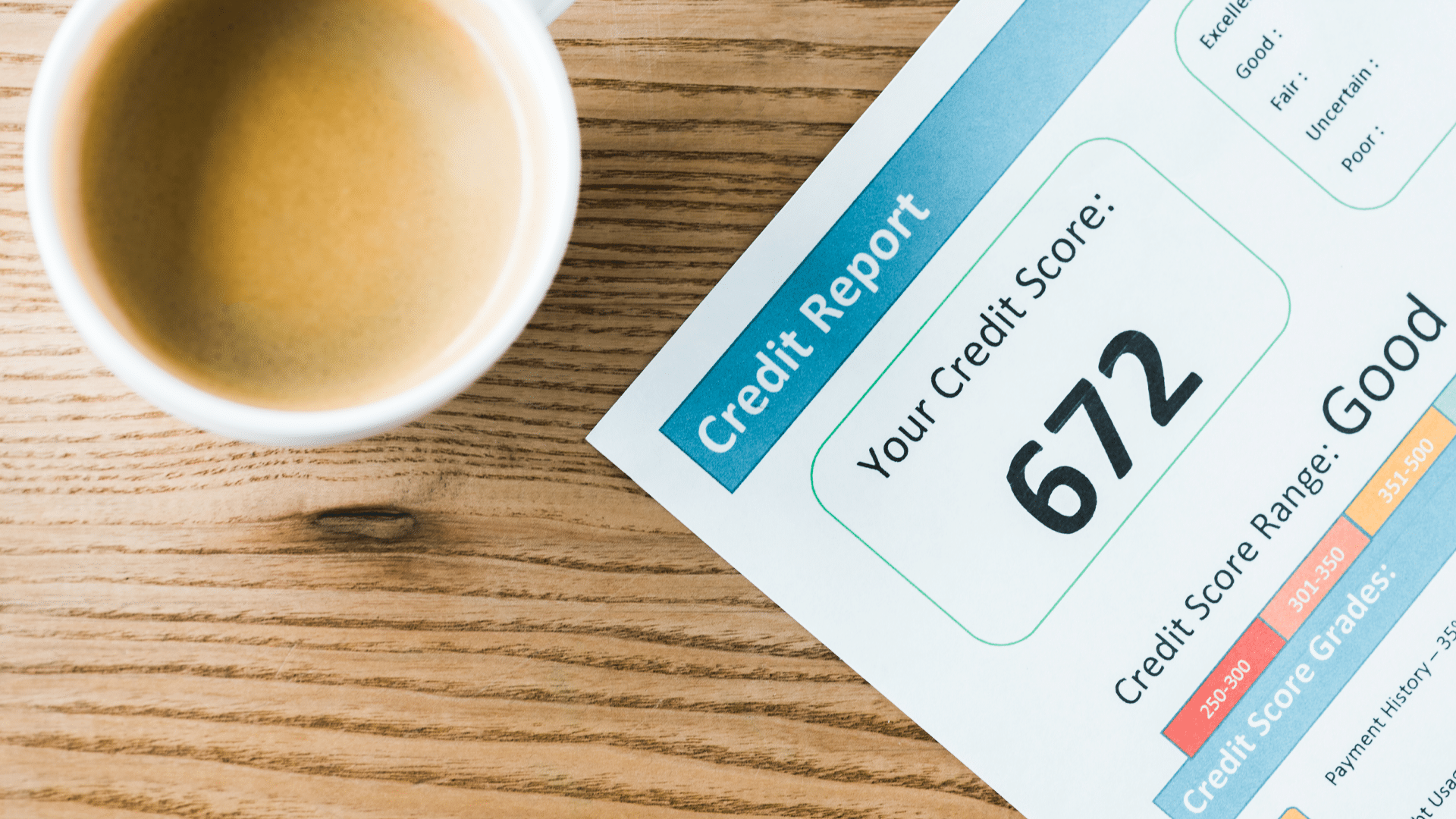

Mortgage lenders assess income on a joint mortgage with parents by considering the combined incomes of all applicants. They will evaluate each party’s income, outgoings, and credit history to determine overall affordability.

Lenders typically use a specific affordability formula to calculate how much you can borrow, factoring in the combined household income. They will also consider each applicant’s financial commitments and debts.

This thorough assessment ensures that the mortgage is affordable for all parties involved, minimising the risk of default.

The difference between joint tenants and tenants in common lies in ownership and the right of survivorship.

Joint tenants share equal ownership of the property and, in the event of one owner’s death, the property automatically passes to the surviving owner(s). This is known as the right of survivorship.

In contrast, tenants in common hold individual shares in the property, which can be unequal. Each owner’s share can be sold or passed on to heirs independently, without the need for other owners’ consent. This setup is more flexible but requires careful planning, especially in terms of inheritance and estate planning.

Getting a mortgage with your parents can be a good idea if you need additional financial support to secure a home. This arrangement can increase your borrowing capacity and help you get on the property ladder sooner.

It’s especially beneficial for first time buyers who may struggle to meet affordability criteria on their own. However, it’s essential to consider the implications, such as the shared responsibility for repayments and the potential impact on all parties’ credit scores.

Speaking with a mortgage advisor can help you weigh the pros and cons based on your specific situation.

Alternatives to joint mortgages with parents include guarantor mortgages and gifted deposits.

A guarantor mortgage involves a parent or close relative guaranteeing the mortgage, meaning they agree to cover payments if you can’t. This doesn’t give them ownership of the property but provides additional security for the lender.

A gifted deposit, on the other hand, involves parents providing a lump sum towards the property purchase, reducing the mortgage amount needed.

Government mortgage schemes such as shared ownership are also viable options for those needing assistance to buy a home.

The drawbacks of having a joint mortgage with parents include shared liability and potential credit implications. Both parties are equally responsible for the mortgage repayments, so missed payments can affect everyone’s credit score.

Additionally, the financial commitment can limit both parties’ future borrowing capacity and flexibility. Parents may also face age restrictions from lenders, which could affect the mortgage terms and conditions.

It’s crucial to have a clear agreement and understanding of the financial responsibilities involved before proceeding with a joint mortgage with a parent. Having a family mortgage is not for everyone; it’s always best to seek mortgage advice first.

Leaving a joint mortgage with your parents typically involves refinancing or selling the property. If you can afford the mortgage on your own, you can apply to remortgage in your name solely, subject to lender approval.

This process will involve a fresh assessment of your financial situation. Alternatively, you and your parents may decide to sell the property and use the proceeds to pay off the mortgage.

Speaking with a mortgage advisor can help you understand the best option based on your circumstances and the lender’s criteria.

The amount you can borrow with a joint mortgage with your parents depends on the combined incomes and financial commitments of all applicants.

Lenders will assess the total household income, including salaries, bonuses, and other sources of income from both you and your parents. They will also consider your outgoings, existing debts, and credit scores to determine affordability.

Generally, having your parents on the mortgage can significantly increase your borrowing capacity, as their income is added to yours. This enhanced borrowing power can make it easier to secure a larger mortgage, allowing you to buy a more expensive property or one that better suits your needs.

Getting personalised mortgage advice is essential when it comes to taking out a specialist mortgage product. The exact amount will vary between lenders, so it’s advisable to speak with a mortgage advisor to get a personalised estimate based on your specific circumstances.

The duration a parent stays on a joint mortgage depends on the terms agreed with the lender and the financial arrangement between the parties involved.

Parents can remain on the mortgage until it is fully paid off or until the child can afford to remortgage independently.

Some parents choose to stay involved for a shorter period, such as until the child’s financial situation improves.

Regular reviews and communication with your mortgage advisor can help determine the best time to adjust or exit the arrangement.

When obtaining a joint mortgage with parents, several legal documents are typically required:

Having these documents in place helps protect the interests of all parties and ensures that the legal and financial aspects of the joint mortgage are clearly defined.

We work around you. Working 7 days a week allows you to pick a date and time that works for you.

Every customer can benefit from a free mortgage appointment with one of our mortgage advisors.

Your case manager will help you prepare your mortgage application and be on hand to answer all of your questions.

Being open and honest is at the core of our service. We will never recommend a mortgage product that does not match your circumstances.

Your mortgage advisor will also recommend insurances to make sure that you and your family are protected from losing your home.

We can access 1000s of mortgage products via high street and specialist lenders. We aim to find the perfect solution for you.

We have over 20 years experience working in the mortgage industry, we're able to help you get a joint mortgage with your parents.

We will be there for you throughout your whole mortgage process, recommending the best mortgage deal for your situation.

Combining incomes with your parents can significantly boost your borrowing power, allowing you to qualify for a larger mortgage.

This means you can potentially afford a more expensive property than you could on your own.

Lenders view the combined income as a stronger financial position, making them more likely to approve a higher loan amount.

With the combined financial strength of both parties, you may be eligible for better interest rates, reducing the overall cost of your mortgage.

Lenders often offer more favourable rates to applicants with higher incomes and lower risk profiles, which can result in significant savings over the whole mortgage term.

Young buyers who might struggle to meet lender criteria on their own can benefit from their parent’s stable income and credit history.

This additional financial backing can help first time buyers pass affordability checks, potentially making it easier to secure a mortgage and get on the property ladder.

Mortgage repayments can be shared between you and your parents, making it easier to manage monthly payments and household expenses.

This shared responsibility can alleviate the financial burden on any single party and ensure that mortgage commitments are met consistently.

Consistently making timely mortgage payments can positively impact your credit ratings, enhancing future borrowing opportunities.

A strong payment history demonstrates reliability to future lenders, which can be beneficial for securing loans or credit in the future.

With a higher borrowing limit, you can afford a better property, possibly in a more desirable location or with more space and amenities.

This can improve your quality of life and provide a more comfortable living environment, which might be out of reach without the joint mortgage arrangement.

Parents can support their children’s homeownership journey without permanently tying up their own assets in the property.

This type of mortgage allows parents to help their children financially while retaining flexibility and not being directly tied to the property in the long term.

Having your parent’s financial backing can provide additional stability, particularly in the early years of homeownership.

This support can be crucial if unexpected financial challenges arise, ensuring that mortgage payments are maintained and the property is secured.

Parents involved in a joint mortgage can exit the arrangement once the child is financially stable enough to manage the mortgage independently.

This flexibility means parents are not indefinitely committed and can step back when their child is ready to take on full responsibility.

Depending on your circumstances, there may be potential tax advantages to a joint mortgage with your parents, such as shared tax relief on mortgage interest payments.

Understanding these benefits can provide additional financial incentives, making a joint mortgage with your parents an attractive option.

Speaking to a tax advisor can help clarify specific benefits and how they apply to your situation.

Read our Reviews

UK Moneyman Limited is Registered in England, No. 6789312

Registered Address: 9 Gallows Lane, Beverley, United Kingdom HU17 7FJ.

Authorised and Regulated by the Financial Conduct Authority.

We are entered on the Financial Services Register No. 627742 at www.register.fca.org.uk.

© UK Moneyman Limited 2025.

UK Moneyman Limited is Registered in England, No. 6789312

Registered Address: 9 Gallows Lane, Beverley, United Kingdom HU17 7FJ.

Authorised and Regulated by the Financial Conduct Authority.

We are entered on the Financial Services Register No. 627742 at www.register.fca.org.uk.

© UK Moneyman Limited 2025.

We value your privacy

This website uses cookies. If you continue to use the site, we will assume that you agree with our use of cookies.